Contents

Konstantin Loshadkin, Anastasia Mikhailova,

Elena Arabova

in Sustainable Resource Use

Moscow State University)

ACKNOWLEDGEMENTS

The creative process is of course the prerogative of the authors. However, the outcome of this process could not have been as complete and as thoughtful without the knowledge and experience of people whose invaluable contribution helped to make the process meaningful, exact and relevant to readers. Our vision of the spatial development of the System of Environmental-Economic Accounting (SEEA) and the related synthesis of concepts and ideas has taken shape since the mid-1990s. Over these years we have had the good fortune to take part in discussions of crucial scientific approaches to the evolution of modern information systems in the relationship between Society and Nature together with authors and academics. We therefore believe that it is important to mention those who have contributed to creating this treatise and bringing it to readers.

We would like to express special thanks to:

Anil MARKANDYA, one of the creators of the concept of the “green” economy. 20 years ago he helped us to master SEEA approaches and methods for applying findings to improve environmental management and regional sustainability. We continue to draw on his forward-looking ideas and to attempt to put them into practice.

Nikolai LUKIANCHIKOV, an outstanding economist in the field of environmental economics, the last Deputy Minister of Ecology and Environmental Management of the USSR, who contributed much to introducing the basic principles of integrated environmental-economic accounting in Russia.

Budimir POYARKOV, who suggested the idea of integrated territorial cadasters of natural resources based on diligent attention to regional and local levels of management.

Henrietta PRIVALOVSKAYA, leader of environmental research in the field of economic geography in Russia who has contributed greatly to the development of our team. Her participation in profound and many-sided discussions helped to clarify and articulate the foundations of our understanding of the territorial synthesis of economic and environmental information.

Konstantin GOFMAN, whose short but highly meaningful and unforgettable talks in the early 1990s on various issues of environmental economics extended our horizons and helped us to embrace various methodological aspects of monetary estimates of environmental resources.

Sergei BOBYLEV, who provided valuable advice on the measurement of sustainable development and economic growth and supported our research in every way.

Renat PERELET, who introduced us to the theory of sustainable development in the early 1990s. and whose friendly support through the last two decades has been of inestimable value.

Vladimir ZAKHAROV, with whom we have had valuable interchanges regarding environmental health and the importance of the Earth Charter.

Miriam LINSTER, who offered numerous timely and highly fruitful recommendations on creating and developing green economy and green growth indices, drawing on OECD expertise.

Vim COFINO for insightful discussions on philosophy and sustainability measurement.

Alexander DUMNOV for valuable consultations on the basic methodology of environmental statistics and specifics of environmental-economic accounting.

Alexander LYUTY, whose “language of maps” helped us finalize the methodological basis for creating behavioral maps integrated with the SEEA and formulating map legends with a focus on sustainable resource use and environmental protection.

We are also grateful to Yuli Lipets, Valery Pulyarkin, Enrid Alayev, Luisa Nochevkina, Vladimir Streletsky, Andrei Treivish, Irina Volkova, Tatyana Runova, Hans-JürgenTaurit, Lev Knyazkov and many other colleagues for their sympathetic and deep discussion of numerous ideas in the course of informal meetings.

At various stages of the work our research was supported by leading experts of the Russian Ministry of Natural Resources and Environmental Protection, the Federal Service for National Statistics, Federal Service for Supervision of Natural Resources, as well as regional and municipal administrations in Kaliningrad, Kaluga, Kemerovo, Kostroma, Nizhny Novgorod, Ryazan, Saratov, Tomsk, Yaroslavl, Kamchatka and Krasnoyarsk Regions, the Republics of Buryatia, Karelia and other subjects of the Russian Federation.

Our understanding of the SEEA principles was greatly expanded by regular participation in meetings on environmental statistics and environmental-economic accounting held by UNECE (Lidia Bratanova, Tiina Luigi, etc.), the UN Department for Statistics and the OECD, where we have refined our views of statistical environmental systems over a period of nearly 10 years.

Our special thanks to Andrey Tatarinov, Natalia Shashlova, Marina Klevakina, Galina Romashkina, Mikhail Gordonov, Alexander Averchenkov, Anatoliy Shevchuk, Olga Medvedeva, Arkady Tishkov, Alexander Adam, Alexander Golub, Alla Shvets, Vladimir Revezensky, Mikhail Buyanov, Elena Bondarchuk, Valery Panov, Margarita Tsibulnikova, Vladimir Morozov and many others for their expert assistance at various stages of the research, on which the conclusions of this book are based.

ABBREVIATIONS

GDP – Gross Domestic Product

GRP – Gross Regional Product

WTO – World Trade Organization

CEA – Classification of Environmental Activities

IAEA – International Atomic Energy Agency

RVM – Residual Value Method

ISIC – International Standard Industrial Classification of all Economic Activities

IEA – International Energy Agency

UN – United Nations

SPA – Special Protection Area

OECD – Organization for Economic Cooperation and Development

SNA – System of National Accounts

EPEA – Environmental Protection Expenditure Accounts

SEEA – System of Environmental-Economic Accounting

SEEA-W – System of Environmental-Economic Accounting for Water

SDG – Sustainable Development Goals

NDP – Net Domestic Product

NPV – Net Present Value

SEIS – Shared Environmental Information System

GLOSSARY

Asset is a store of value representing a benefit or series of benefits accruing to the economic owner by ownership or use of the asset over a period of time. It is the means of transferring value from one accounting period to another (Central Framework for the SEEA. UN, 2012).

Man-made (physical) capital includes man-made means of production, such as machines, buildings, production infrastructure, which are involved in the production process without being materialized in the final product (Renat Perelet. Systems Management of Transition to Sustainable Development, 2009).

Return on Produced Assets is the income from the use of produced assets in the process of production after deduction of the fixed capital consumed in this process (Central Framework for the SEEA, UN, 2012).

Return on Environmental Assets is the income attributable to the use of environmental assets in the production process after deducing all costs of extraction including any costs of depletion of natural resources (Central Framework for the SEEA. UN, 2012).

Living System is a multiple interconnected network whose components continually change, are transformed and are replaced by other components. The network is characterized by exceptional flexibility and fluidity, which enables the system to respond in a specific way to disturbances or “stimuli” coming from the environment (Capra, F. The Web of Life. A New Scientific Understanding of Living Systems. Moscow: Sofia Publishing House, 2003).

Green Economy is the economy, which serves to improve human well-being and social equity, while significantly reducing environmental risks and ecological scarcities. The green economy is a system of economic activities related to the production, distribution and consumption of goods and services, which results in long-term improvement of human well-being without exposing future generations to significant environmental risks and ecological deficits; it is environmentally harmless, eco-friendly and socially fair (Towards a Green Economy: Pathways to Sustainable Development and Poverty Eradication. UNEP, 2011).

Green Growth involves fostering economic growth and development while ensuring that natural assets continue to provide the resources and environmental services on which our well-being relies. This is achieved by catalyzing investment and innovation to underpin sustained growth and create new economic opportunities (Towards Green Growth. A Summary for Policy Makers. OECD, 2011).

Inclusive Growth is a new approach to understanding economic growth, focused on improving living standards and achieving more equitable distribution among social groups of benefits from increased well-being (All on Board. Making Inclusive Growth Happen. OECD, 2014).

Institutional Unit is an economic entity that is capable, in its own right, of owning assets, incurring liabilities and engaging in transactions and other economic activities with other entities (Central Framework for the SEEA. UN, 2012).

Use of Natural Resources is the exploitation of natural resources, their transfer to economic activity, including any way of affecting them in the process of economic or other activity (Federal Law of 10.01.2002 No. 7-FZ (as amended on 29.12.2015) “On Protection of the Environment”).

Cultivated Biological Resources include animal resources yielding products on a regular basis, as well as timber, crop and plant resources yielding repeat products on a regular basis, whose natural growth and regeneration are under the direct control, responsibility and management of an institutional unit (Central Framework for the SEEA, UN, 2012)

Best Available Technology is a technological process or technical method based on advanced scientific and technical achievements, which is aimed at reducing negative environmental impact of economic activities and has an established service life with due account for economic, technical, ecological and social factors (Amendment No.1 GOST P 521004-2003 Resource Saving Terms, Definitions approved by Rosstandart Order of 30.11.2010 No.756-st)

Negative Environmental Impact is the effect of economic and other activities resulting in negative changes in the environment (Federal Law of 10.01.2002 No.7- FZ (as amended on 29.12.2015) “On Protection of the Environment”).

Non-Produced Assets are assets that have come into existence in ways other than through processes of production. (Central Framework for the SEEA, UN, 2012).

Environment is a complex of the components of the natural environment, natural, and part-natural, part-man-made objects as well as man-made objects (Federal Law of 10.01.2002 No. 7-FZ (as amended on 29.12.2015) “On Protection of the Environment”).

Fixed Assets are produced assets that are used repeatedly or continually in production processes over a period longer than one year. (Central Framework for the SEEA. UN, 2012)

Natural Resources are components of the natural environment, natural objects and part natural-part man-made objects which are used or can be used in economic or other activities as energy sources, production outputs and for consumption, and which have consumption value. (Federal Law of 10.01.2002 No.7-FZ (as amended on 29.12.2015 “On Protection of the Environment”).

Environmental Capital (in terms of the theory of economic growth) is the aggregate of natural resources, which can be used in production processes. Any environmental asset creating a flow of eco-services with economic value is environmental capital (Dictionary of Sustainable Development Terms, http://www.ustoichivo.ru)

Environmental Institutions are the “rules of the game” in a society, a certain framework of limitations that organize relations between individuals with due account for environmental factors. Such institutions are the products of collective effort; they generate incentives that induce people to comply with environmental restrictions and regulations. They reduce uncertainty by structuring everyday life or, in other words, they determine or limit the range of alternatives available to each individual in his or her relations with the natural environment. Environmental institutions make the behavior of people and communities in the environmental sphere more predictable, reducing the probability of destructive behavior and conflicts caused by it (Fomenko, G.A. Environmental Management: A Socio-Cultural Methodology. Institute for Sustainable Innovation, San Jose, 2017)

Produced Assets are assets that have come into existence as outputs of processes that fall within the production boundary of the SNA. (Central Framework for the SEEA. UN, 2012)

System of National Accounts is an internationally coordinated standard set of recommendations to measure indicators of economic activities in accordance with strict rules of accounting and reporting at the macro level based on the principles of economic theory (System of National Accounts 2008. New-York, 2012 p. 64)

System of Environmental-Economic Accounting is a multipurpose conceptual framework for describing the interaction between the economy and the environment and the stocks and changes in stocks of environmental assets. (Central Framework for the SEEA. UN, 2012)

Bifurcation Point is a critical state of the system when the system becomes unstable in respect of fluctuations and uncertainty arises whether the state of the system will become chaotic or whether it will ascend to a new, more differentiated and elevated level of regularity (Muzika, O.A. Bifurcation in Nature and Society: Natural-Science and Socio-Synergetic Aspect // Modern High Technologies 2011. №1 С. 87-91).

Sustainable Productivity is an excessive or surplus quantity of animals or plants, which can be absorbed from the population without affecting the capacity of this population for self-reproduction. (Central Framework for the SEEA. UN, 2012)

Sustainable Development is development, which can meet the needs of the present generation without undermining the ability of future generations to meet their own needs (Our Common Future. Report of the International Committee on Environment and Development. 1987. Moscow: Progress, 1989)

Vulnerability of Environmental Systems is the inability of environmental systems (biological communities, landscapes, etc.) to withstand the impact of external forces (any forces, although man-made effects are of special significance). Vulnerable environmental systems can be easily disturbed; they can lose their structure and function, and may be rearranged in a harmful way (Malashevich Ye.V. Short Reference Dictionary on Environmental Protection. Minsk, 1987)

Environmental Assets are the naturally occurring living and non-living components of the Earth, together constituting the biophysical environment, which can provide benefits to humanity (Central Framework for the SEEA. UN, 2012)

Environmental Risk is the probability of occurrence of an event having unfavorable consequences for the natural environment, caused by negative impact of economic or other activities, or by emergencies of an environmental or man-made character (Federal Law of 10.01.2002 No. 7-FZ (as amended on 29.12.2015) “On Environmental Protection”).

Ecosystems are geographical locations that host a dynamic complex of plant, animal and microorganism communities and their inorganic environment, interacting as a functional whole to generate environmental structures, processes and functions (the Central Framework for the SEEA. UN, 2012)

Ecosystem Services are the functions of ecosystems in providing benefits to the users of such services through the natural achievement of various kinds of regulating functions. Users of the services may be at local level (individual enterprises), or at regional or global level, including entire countries and regions (Convention on Biological Diversity – International Agreement adopted in Rio de Janeiro on June 5, 1992).1

FOREWORD

Unprecedented in terms of its historical importance, the adoption of universal global sustainable development goals (SDGs) has produced a corresponding demand for information and analytical support in achieving these goals.2 In instrumental terms, the comprehensive nature of SDGs requires a change in approaches to strategic environmental planning and program-oriented and goal-oriented management at all levels of territorial organization. In methodological terms, it means the enhancement of coverage and the goal-oriented shift of focus in addressing problems of territorial development at all stages of work with information resources, starting from data selection, generalization, analysis, interpretation and understanding, which, in fact, means a substantial change in approaches to creation and further development of information and analytical support. Alongside tackling data systematization and update challenges for the purposes of addressing management issues, a special emphasis should be placed on the goal-oriented synthesis of sustainable development and green economy indicators, environmental indicators and special socio-cultural measurements.

In our opinion, the nature of discussions around SDGs and how they can be achieved reflects the changes that are occurring in understanding of the use of natural resources and, more broadly, the very essence of nature, not only as a set of natural objects and resources but also in its system “integrity” (Cassirer, 2004). The importance of these discussions correlates with the fact that by the end of the 20th century, the “wholeness” of nature has been considerably rethought, primarily, in the context of phenomenological philosophy and sociology. Alfred Schütz submitted an important argument that a distinction must be drawn between nature as a discipline of natural sciences and nature as a “constructive element of the lifeworld” (Schutz, 2004). As a result, at the worldview level, it further justified the occurring changes in views on the reasonability of broad application, in the context of sustainable development, of the theory of utility and full economic value to natural resources and ecosystem services, which predetermined new information needs.

On the other hand, the adoption of the sustainable development goals (SDGs) itself has become possible due to the emergence and rapid development in the last years of instrumental methods for collecting and processing enormous amounts of empirical data (including those at the micro-level, including aggregation and disaggregation, various interpretations in accordance with the set objectives, etc.) accumulated by behavioral and social sciences and representing the characteristics of the described essences for the purpose of their identification, search, assessment and management (American Library Association, 1999).

The key problem of environmental and economic measurements is that of measuring the sustainability of the use of natural resources (which, in fact, this book is addressing). We, the authors, proceed from the fact that the modern theory of sustainable development constitutes the most developed and acceptable methodological basis for maintaining Peace and preventing a global environmental disaster. Today, the System of Environmental-Economic Accounting (SEEA) provides the best way of measuring the key interactions between the economy and the environment.

As geographical scientists, we grew in the Russian cultural environment with its ambition for comprehensiveness and indivisibility of the world perception. These socio-cultural peculiarities of the vision (as well as the authors’ multifaceted work experience in management, production, design structures) allow perceiving naturally and to use the multidisciplinary approach to research that is quite productive in finding paths to sustainable development. It should be noted that our understanding of territorial planning and holistic accounting for natural resources and ecosystem services was formed by the Russian geographical school. It also must be mentioned that it was a good school of holistic territorial accounting for natural resources. However, behavioral specifics of communities, monetary relations, especially in the context of resource use preferences driven by socio-cultural factors, were significantly limited by the then dominating labor cost theory that hindered development of the behavioral economy and institutional geography.

In the early 1990s, it could be seen particularly well. The lack of monetary assessment of natural resources and the environment inherited from the state-planned and command system became one of the cornerstone problems of effective use of natural resources. In the new situation, when businesses no longer took into account the environmental and social requirements of territorial development of regions and settlements in locating their new manufacturing sites, the task of system accounting for natural resources to ensure multifaceted management and strategic planning of territorial development became more challenging.

Despite the economic difficulties in the Russian Federation, holistic environmental-economic accounting activities began in 1990s because information systems inherited from the state-planned and administrative system were set to collect information on key types natural resources and to address particular industrial issues. They did not allow conducting territorial analysis for comparing the real value of natural assets with income gained from their use, nor to conduct retrospective and forecasting research (including assessment of depletion of economically significant natural resources), nor to compare the value of various components of natural wealth (when planning investment). Moreover, the then existing information flows did not cover a wide range of natural resources; comparison of results was complicated due to the differences in collection, processing and visualization methods. Under such conditions, it is extremely difficult to justify and make effective management decisions on the multipurpose use, reproduction and protection of natural resources.

Our organization (Cadaster Institute), a scientific and production enterprise of cadasters of natural resources, was established by the Ministry of Environmental Protection and Natural Resources in the Russian Federation in 1992. Special attention in methodical and practical developments was paid to assessment of socially and environmentally dangerous exhaustibility due to extraction or quality deterioration of a resource as a result of economic activities (in physical and value, i.e. monetary, indicators); establishment of indicators of stocks and use of natural resources and ecosystem services not accounted in the existing statistical monitoring and departmental accounting systems; institutional aspects of the use of such indicators, including those driven by socio-cultural factors.

Today, we can identify the following stages of development of this area in the Russian Federation.

Stage One: the conduct of the federal experiment for improvement of accounting and socio-economic assessment of the natural resource potential (1993-1995). It was based on an attempt to develop and implement Integrated Territorial Natural Resources Inventories in environmental management practices. The experiment for developing Integrated Territorial Natural Resources Inventories was conducted under the guidance of the Ministry of Environmental Protection and Natural Resources of the Russian Federation in 35 constituent entities of the Russian Federation and was developing quite successfully. Two all-Russian meetings were conducted at the premises of Cadaster Institute in 1992 and 1994, where the experiment results were discussed.

Integrated Territorial Natural Resources Inventory was initially planned to contain data on natural resources in physical terms and could serve as a basis for their assessment in the structure of the regional and, ultimately, national system of environmental-economic accounting. Economic assessment was considered a necessary completing link in the system of holistic cadastral assessment of natural resources allowing inclusion of natural assets into assessment of economic activities. It was expected that such assessment would give an objective idea of the economic value of natural resources and allow justification of investment in their reproduction and protection and to select the most effective way of using such resources.3 In case of multipurpose use of natural resources, their monetary estimates could allow not only choosing how to use a particular resource (object) but also determining a strategy for sustainable use of the natural resource potential of the entire territory. Furthermore, they hoped that monetary estimates of natural resources could help optimize taxation of various types of natural resource use.

Stage Two: development of the regional environmental-economic accounting operations in accordance with the UN methodology (1996-2006). By that time, the flaws of the methodology of multipurpose territorial cadasters of natural resources had become apparent. They included the loss of the modern geographical science integrity: the unity of natural sciences and humanities in geography was split into many disciplines while physic-geographic and economic-geographic branches diverged substantially. Thus, in methodological terms, the very structure of measurements in the system Society-Nature that could allow creation of multifaceted geographical description within Integrated Territorial Natural Resources Inventory turned out to be weakly developed. During the development of Integrated Territorial Natural Resources Inventories, the static nature of most indicators reflected in them (stocks of natural resources, production, emissions and discharges, etc.) was discovered, which became an obstacle in analyzing the efficiency of regulation in natural resource use and environmental protection. The need has become obvious, not only in the system territorial approach allowing for economic comparison of natural resource use options but also in the dynamics — changes in raw material flows and ecosystem services, including in monetary terms.

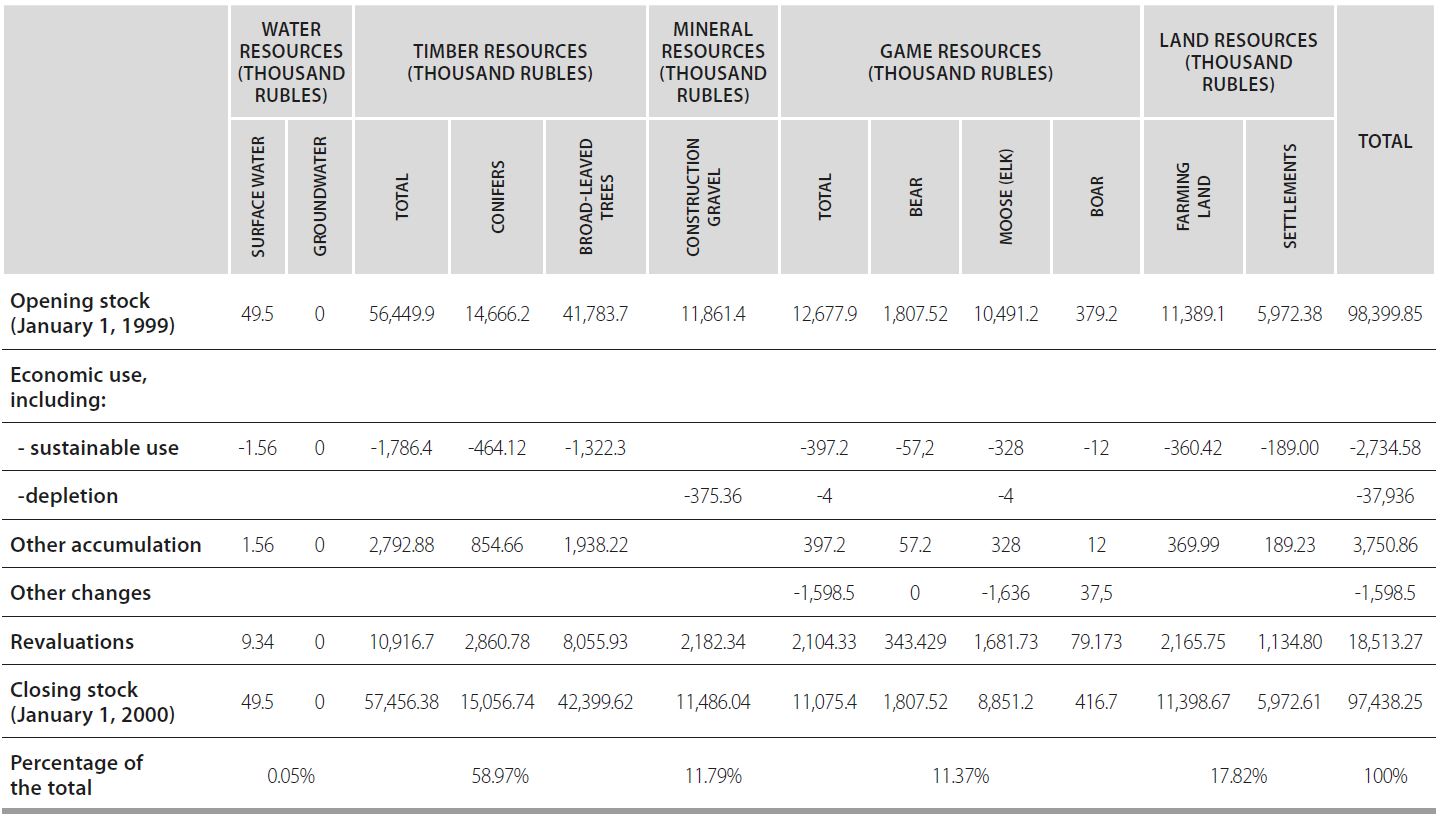

Many other countries faced similar problems. It became possible to move forward owing to the System of National Accounts (SNA) and its satellite System of Environmental-Economic Accounting. The latter is a set of interrelated statistical indicators reflecting the state of natural capital (stocks, flows and other changes), allowing adequate determination of the value of natural resources and inclusion of it into the balance sheets of assets and liabilities within the framework of SNA. The System of Environmental-Economic Accounting is actively developing in many countries. A considerable contribution to establishment of the SEEA in the Russian Federation was made by the world-renowned scientist, Professor Markandya, one of creators of the very idea of “green economy” (Pearce, Markandya & Barbier, 1989); he personally consulted us during the initial stage of works in 1994-1999 (Fomenko, G., Fomenko, M., Markandya, & Perelet, 1997b). Development of the System of Environmental-Economic Accounting of the Yaroslavl Region should be deemed basic. As a result, based on the analysis of data on the availability and economic use of main natural resources (surface water, soil water collected from public water supply systems, ground water collected from wells, agricultural lands, timber and non-timber forest resources, recreational areas, hunting, fishing, mineral resources — sand and sand-gravel mix, bee resources), for the first time in Russia, the SEEA matrix was created, the amount of natural capital of the Yaroslavl Region was determined, the regional green GDP and NDP were calculated. As the research results has shown, the assessment of natural assets allows determination of the effectiveness of the current scenario of natural resource use (public water supply, forest, mineral resource complex, etc.) and to identify the most efficient areas of sustainable development.

Later, with the support of the Ministry of Natural Resources of the Russian Federation, the Federal Service for Supervision of Natural Resources Use and its territorial bodies as well as governmental and local self-regulation authorities of the Republic of North Ossetia-Alania, the Republic of Karelia, the Tomsk, Ryazan, Kaluga, Saratov, Kaliningrad and Kostroma Regions, the positive experience gained was used in other regions of the country. The emphasis was placed both on accounting for natural resources in physical terms and on economic assessment of natural resources. It was due to the extremely high role of the SNA/SEEA as a tool of analysis of socio-economic development in many countries.4

Not only did the results of regional research confirm practical applicability of the UN methodological principles of environmental-economic accounting in Russia and demand for obtained results in environmental management but also detected gaps in statistical and departmental information. First of all, it was the lack of indicators characterizing stocks and flows of natural resources (quantitative and qualitative aspects). Ineffectiveness of the territorial analysis based only on the “top-down” approach has become apparent. In the course of the works, it was supplemented by the “bottom-up” approach implying clarification of regional indicators of availability and actual consumption of natural resources at the municipal district level (starting from local settlements and private households, with further aggregation of this data at higher levels of territorial organization).

Stage Three: work activation at the federal level based on the territorial approach (2007-2011). At this stage, we conducted a pilot study to assess the possibility of application of the SEEA basic methodology at the federal level.5 The study was conducted in accordance with the provisions of international methodological documents on accounting for the value of natural assets in national wealth.6 More than ten years of experience in monetary assessment of natural resources in accordance with the SNA/SEEA approaches enabled us to conduct in Russian regions the analysis of conceptual approaches to recording natural resources in the SNA as a part of financial assets and establishing a satellite system of environmental-economic accounting. The state statistical monitoring system in use of natural resources and environmental protection was analyzed in terms of compliance with the SNA principles, and the methodology for valuating natural resources was summarized in accordance with the SNA/SEEA requirements.

These studies allowed development of methodological principles of recording the monetary estimate of natural wealth in the statistical system. With the support of Rosstat (Federal State Statistics Service), the SEEA matrices were completed, for the first time, by constituent entities of the Russian Federation. In our opinion, for Russia, such disaggregation is crucial because timely identification of dangerous trends of natural capital depletion, in both monetary and physical terms, is especially important for regions. The results obtained visibly intensified activities of accounting for natural assets in national wealth within the framework of the Federal Target Program “Development of the State Statistics in 2007-2011.”7 This program envisaged improvement of statistical monitoring of the use and replenishment of natural resources and environmental protection based on the effective system of indicators and methodology of their establishment.

Stage Four: assessment of the country’s natural capital based on the industrial approach (2012 until present). The development of works in the Russian Federation was based on the following documents:

1) System of National Accounts, 2008, Central Framework of the System of Environmental-Economic Accounting, 2012, System of Environmental-Economic Accounting for Water, 2012;

2) Roadmap for Accession of the Russian Federation to the OECD Convention adopted at the 1163rd session of the OECD Council of November 30, 2007;

3) Decree of the Government of the Russian Federation (October 12, 2012 No.1911-r) on Making Amendments to the Federal Plan of Statistical Works Approved by the Government of the Russian Federation (May 6, 2008 No.671-р);

4) Action Plan to Perform Works Envisaged by the Decree of the Government of the Russian Federation (October 12, 2012 No.1911-r), in respect of the monetary estimates of natural resources and calculation of resource efficiency (Order of Rosstat of July 8, 2013 No.274).

Under the guidance of Rosstat, methodological recommendations were prepared on economic assessment of water, mineral resources, ground and water bio resources in the SNA. In this area, in 2014-2015, the Cadaster Institute developed “Methodological Recommendations for Economic Assessment of Forest and Hunting Resources (as Non-Cultivated Biological Resources),” covering the following:

1) key concepts of forest and hunting resources as non-cultivated biological resources in terms of their assessment as a part of natural capital in accordance with the SNA/SEEA principles;

2) the SNA/SEEA methodological approaches in relation to the general principles and peculiarities of assessment of these resources at the current market value in the institutional conditions and statistical reality of the Russian Federation;

3) procedure for conducting calculations in assessment of forest (timber and non-timber forest products) and hunting resources and calculation of the resource rent and discounted value of non-cultivated biological resources (Fomenko, G., Fomenko, M., Loshadkin & Arabova, 2016).

The work conducted is particularly topical due to the introduction of a range of statistical indicators of stocks of non-cultivated biological resources (timber and animals, in physical terms and current market prices as of the beginning and the end of the year), changes in non-cultivated biological resources starting from 2016 and indicators of the use of non-cultivated biological resources in the economy, in physical terms and current market prices, starting from 2019.8

Our work on this book was designed to demonstrate our vision of ways and specific features of development of information systems in natural resource use and environmental protection using SEEA. For this purpose, we deemed necessary to provide the philosophical and methodological framework for establishing and developing the SEEA based on the theory of living self-organized systems; to show the essence of the SEEA, including its origins and development, its place and role compared to other information systems, its institutional and organizational peculiarities; to describe the experience of implementing the SEEA provisions in Russia; to demonstrate, on the example of a number of projects, the effect of the results of assessment of environmental resources and ecosystem service on addressing complex issues of natural resource management and strategic planning of territorial development; to describe the SEEA development paths. Our aim was to take into account the new requirements for SNA/SEEA development to the maximum extent possible, to present some of our conclusions and observations, to make the material useful for a wide circle of experts and practical specialists.

METHODOLOGICAL PREMISES. SIGNIFICANCE AND BASIC PROVISIONS OF SNA/SEEA

In today’s dynamic world the concept of sustainability increasingly implies, not so much stability, as the ability of systems to survive, adapt and develop under the impact of unpredictable changes or even catastrophic events. In order to achieve sustainable development, i.e., to attain well-being within the limits of the planet’s environmental potential, there has to be a radical change in existing patterns of production and consumption, which are the root cause of hazardous impact on the environment and climate. Such changes depend upon profound transformation of principal public institutions, practical approaches, technologies, politics, lifestyle and thinking.

The attainment of a new level of stability requires green innovation, quality forecasting and new effective partnership between corporations, governments, territorial communities and other stakeholders. Sustainable control by government over environmental, social and economic development depends on obtaining and analyzing relevant scientifically based and officially substantiated information timely. The required information includes, in addition to environmental indicators, data on the stocks of various kinds of natural resources, which are essential components of the environmental capital of a region or country, on the manner and intensity of their use in the economy, the yields obtained, etc.

The declaration of global goals of sustainable development in 2015 will entail change in approaches to strategic environmental planning and management by objectives at every level of territorial organization. Methodologically, this means expansion of scope and shift of focus at all stages of information handling, starting from the choice of required data, their generalization, analysis and interpretation, entailing the need for a new approach to the provision of information and analysis. In turn, that provision depends on a goal-oriented synthesis of the indicators of sustainable development and the green economy, of environmental indicators and specific socio-cultural measurements. The key element of the new information synthesis is a definition and substantiation of the core platform, which is adequate to the needs of today.

Measurement has paramount importance in the theory of sustainable development. As early as the 15th century Nicholas of Cusa, who was a forerunner of the scientific perception of the world, believed that humans can cognize nature by means of their senses, imagination, reason and intellect. “Reason, from the moment that its nature admits speculation, perceives only the universal, the incorruptible and the unceasing.” In his treatise The Layman on Wisdom and the Mind he states the need to develop precise methods of measurement, particularly mathematical measurement (Nicholas of Cusa, 1979). Nicholas of Cusa believed correctly that the cognition of genuine essences is not possible, or can only be attained by more or less accurate conceptions. He advocated the concept of learned ignorance: even the deepest knowledge does not eliminate ignorance.

Changing the World View The following points are important for an understanding of the nature of the changes now affecting information support for resource use and environmental protection.

First of all, at the start of the third millennium the world community is increasingly conscious of the global character of environmental problems and the real possibility of the occurrence of environmental crises (not just regional but also global), and also understands the responsibility of humankind for any such developments.

Secondly, recognition of the threat of environmental catastrophe and the impossibility of preventing it by means of technology or economic mechanisms alone has led to a reconsideration of many conceptions, including those concerning the relationship between Society and Nature. Many outstanding thinkers and philosophers of the 20th century (Teilhard de Chardin, Vernadsky, Fromm, Jaspers, etc.) insisted that the development of society could not progress further without changes in the existing paradigm of the relationship between human and nature. It is no coincidence that the late 20th century saw the philosophy of environmental crisis develop into a separate branch of philosophical study. According to Hösle, “... the philosophy of environmental crisis must determine the place of this (environmental – Auth.) threat within the philosophy of the history of human culture.”

Schelling’s subject-object approach, which introduces a perception of the essence of nature in its entirety and not just as a collection of natural objects and resources, is of particular importance for proper understanding of today’s world. We would note that nature as “wholeness” has been substantially reconsidered in phenomenological philosophy and the sociology of resource use. Precisely the phenomenological view of nature, a new understanding of the basic difference between nature as a constituent element of the “world as experience” and as a store of resources had made it possible to methodologically substantiate the importance of evaluating natural resources and ecosystem services in their broadest sense.

This perception of the world has been developed by the new systemic concept of life (Bogdanov, von Bertalanfi, Prigozhin, Maturana and Varela, Capra, Kuznetsov, Moiseev, etc.) The new paradigm is often called holistic, which emphasizes its view of the world as an integrated whole. It focuses on the complexity of “systems” views and introduces new key concepts, such as self-organization, social communication networks, development as a systemic process.

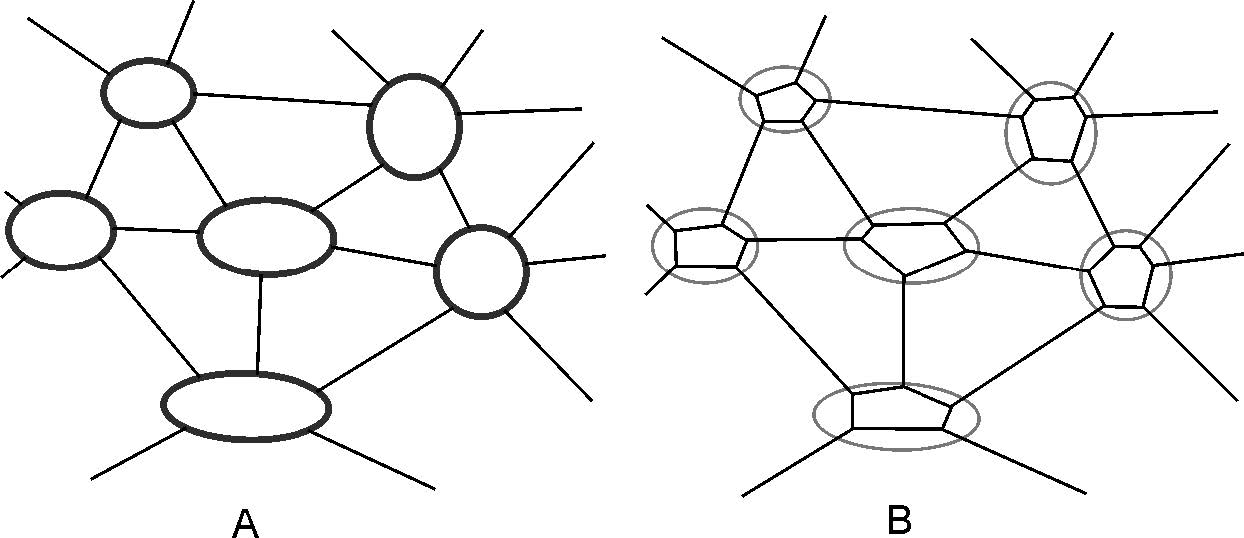

In this concept the essential properties of an organism or a living system are properties related to the whole which are not inherent in any of its parts. There has been a change in the conception of the relationship between parts and whole. In the systems approach, the properties of the parts can only be deduced from the organization of the whole. Accordingly, the systemic approach focuses on main principles of organization rather than on “building blocks.” Capra noted that Systems Thinking is contextual thinking; and since to explain things in terms of their contexts is to explain them in terms of their environment, all systems thinking is a philosophy of the environment. Shifting focus from the parts to the whole can be seen as a transition from objects to relationships. According to the mechanistic world view, the world is a collection of objects. They inevitably interact with each other, hence there are relationships between them. However, the relationships here are secondary, as shown schematically in diagram A (Fig. 1.1). Systems thinking proceeds from the idea that objects themselves are networks of relationships included in bigger networks. For the systems thinker, relationships are primary. The boundaries of various patterns (“objects”) are secondary, as shown in diagram B (Fig. 1.1)

By presenting the living world as a network of relationships, network thinking (more elegantly, in German, vernetztes Denken) has become another key aspect of systems thinking (Capra, 2004). Such a philosophical and methodological position does not permit the human being to be thought of as a creature who has accidentally “fallen out” of the natural world that surrounds him or even become its natural adversary.

The adoption of the global goals of sustainable development9 assumes the description of future events as “must do,” setting radically new methodological problems for environmental work (in a broad sense)10 , based on the goal-oriented synthesis of natural, humanitarian and technical expertise. This enhances the role of environmental ethics which, according to Jonas, must gradually become “future-oriented ethics” (Zukunftethik): the current situation requires “far-sighted forecasts, broad responsibility (for the future of humankind) and large-scale vison (the whole future essence of human) as well as ... harnessing the power of technology to the greatest possible extent” (Jonas, 2004).

Here, the ethics of preserving life acquire an ontological sense, as described by Kant, Fichte, Hegel and, in particular, Schelling, and renounce the strict opposition of subject and object11 . On the one hand, the human being is produced by nature and thus is an integral part of nature. On the other hand, the human is the only living being capable of cognizing the principles of its own existence and evolution as well as those of nature. This duality, according to Schelling, is the enigma that any theory of the human-nature relationship has to address. Schelling was described by Bulgakov (2009) as a “philosopher of nature and objective reality.” Two profound and vital ideas put forward by Schelling are of the utmost importance today for the theory of sustainability:

1) identity of subject and the object in their dynamic development;

2) understanding of nature as a living, evolving organism, corresponding to the concept of “Gaia,” when the Earth was treated as a living being.

E. Laszlo (1997) was therefore correct in stating that the environmental ethics of anyone who strives to enhance biosphere potential for supporting human life are inevitably anthropocentric. A human being should not, however, be unreasonably anthropocentric, because people as a biological species are endowed with the natural capability (and hence the natural right) to strive for collective survival. Individual and social behavior must be oriented to complying with the paramount requirement: to maintain favorable conditions in the biosphere by enhancing people’s responsibility for their actions that affect the natural world. Recognition that nature itself has rights means that people must eliminate intended and unintended negative consequences of their actions for the natural world and be liable for their actions.

Schelling’s subject-object natural philosophy, which endows the natural world with its own dignity irrespective of the human self-development process, is of great significance for sustainable development today. In this perspective the natural world appears as something meaningful, combining the true, the good and the beautiful, worthy of honor and love from human beings as an image of the absolute rather than as something, which they have constructed. Methodological engagement with the interaction of ethics and economics in respect of environmental work is furthered by the ethical economics developed by Kozlovsky. His work offers a deeper insight into the role of ethical codes and religions as guarantors of an ethical approach to nature. Also of importance for understanding the humanistic essence of sustainable development are the views of Bulgakov, while works by Jonas and Hesle are of great significance for the philosophy of environmental crisis, particularly for substantiating the imperative of “responsible behavior.”

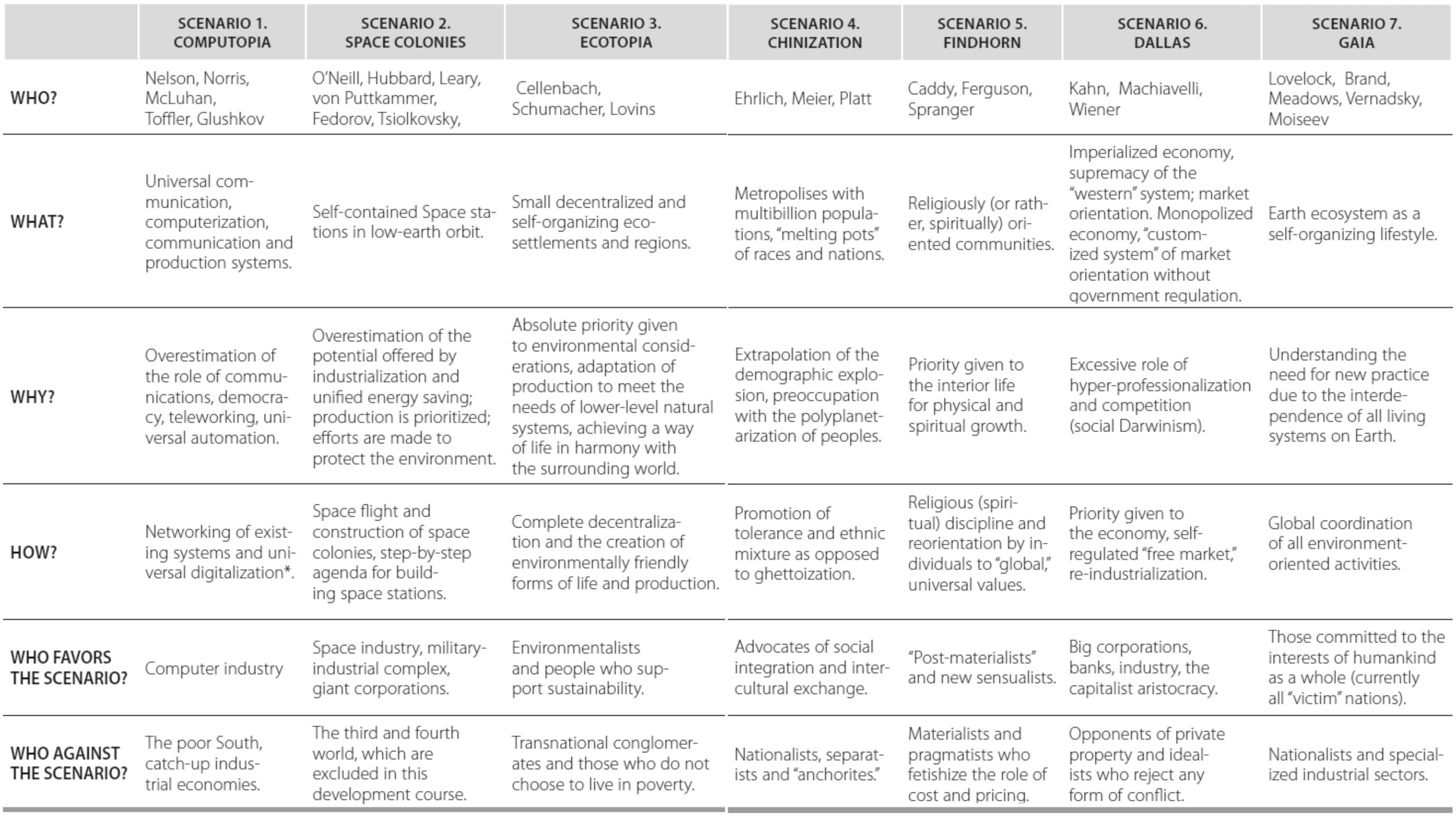

Admitting a Multivariate Future. Any human practice, and particularly that relating to the environment, focuses on a transition from the past to the future that appears reasonable to decision-makers. Possible alternative futures are determined by the synthesis of socio-cultural traditions and trends and tendencies spurred by modernization processes. One of the shrewdest typologies of future scenarios was suggested by Lutz in 1988 (Table 1.1).

Table 1.1 Brief characteristics of main future scenarios

* Digitalization means the conversion of information into discrete forms and its subsequent use to generate numerical indicators

Even looking at the main conceptual trends very generally, substantial differences between their proponents and opponents are evident as regards priority goals, approaches and methods. There is clearly a broad variety of views on environmental priorities, the efficiency of environmental institutions, information support, etc.

It is impossible to predict which scenario will be realized since too many factors are at play and some of them are a matter of chance. It is only possible to identify the causes that have led to the realization of a certain scenario and to discover its logic in retrospect. All that one can do when making forecasts is to list a range of possibilities, identify more and less probable options and determine which of the probable scenarios are particularly hazardous for specific countries and nations, and for mankind as a whole.

The fundamental right of people to choose their own future must be acknowledged unless their choice is evidently destructive for mankind as a whole. For this reason all contemporary definitions of sustainable development, starting from the definition given by Bruntlann12 , proceed by stating what has to be done in order to avoid the most undesirable future scenarios. In other words, a range of acceptable solutions for a country or nation is determined by applying global indicators for human impact on the environment.

Responsible behavior capable of preserving the life of present and future generations must focus on preventing global environmental catastrophe, mitigating risks and preventing conflicts in the sphere of environmental management at minimum cost. Devising and implementing approaches to sustainable development depends on finding ways forward and limitations in the regulation of social, natural and systems, and means of purposeful impact on these systems in response to growing development risks in a production-oriented society.

Since spatiality is one of the fundamental dimensions of human existence, structuring our world outlook and action, it makes sense to speak of a space of risks, including environmental risks, at all levels of territorial organization (both explicit and implicit). This is, essentially, a geographical space treated in terms of riskology and distinguished by territorial characteristics, generating an aggregate of relationships between geographical objects in a specific territory evolving over time (Environmental Institutions, 2010). In this approach the measurement of environmental risks and respective indicators must be included in any evaluation of the territory’s natural capital.

Changing the concept of “sustainable resource use.” Contemporary philosophy tends to affirm multiple forms of rationality. According to the concept of the unity of rationalities, scientific, philosophical, religious and other rationalities are not alternatives but aspects of a single and multifaceted mind. It is therefore wrong to be skeptical about other forms of rationality that are characteristic of other civilizations and nations, or of other historical periods. In particular, the idea of transformation of the natural world and its harnessing to human needs has prevailed in western culture in all periods of its history up to the present. However, the same idea is virtually absent in traditional cultures where the relationship of people to the world around them has been understood and evaluated from completely different positions: an inherent conservatism, slow rates of evolution of human action, and the predominance of traditional means of environmental regulation have constrained the transforming power of human beings.

The most acute value-based conflicts arise from differences in the understanding of “rational behavior” as regards environmental management and nature conservation. In our view, in order to ensure sustainability and prevent conflicts escalating to a critical level, emphasis has to be placed on people’s responsibility for their own future and the future of mankind as a whole. Jonas maintains that the concept of homo sapiens (“reasonable human being”) should be substituted by that of homo responsabilis (“responsible human being”), and traditional ethical systems should be substituted by a new ethics – the ethics of responsibility. The imperative addressed to the new types of actors must, according to Jonas, be “Act so that the effects of your action are compatible with the permanence of human life” (Kane & Osantowski, 1981). This idea is in tune with the views of Ladd who suggested that responsibility should be considered the essential feature of a human being: “People are beings who understand their actions and who are responsible for the consequences of their actions” (Ladd, 1975). A person who bears responsibility for achieving the sustainable development goals of mankind13 , or of his or her country and local community needs adequate information about the state of the Society-Nature system and real development trends.

Main implications for the SEEA arising from the systems concept of life, recognition of a multivariate future and multiplicity of rationalities. Changes happening in the world today point to a number of new ways, in which information can be usefully employed to support sustainable resource use and protection of the environment.

-

Work to reform the information and statistical systems, which describe relationships in the complex non-linear Society-Nature system, must bear in mind that, in the systems approach, we must measure relationships rather than objects, and particularly relations between ecology and the economy at all levels of territorial organization. The SEEA can be described as an organizationally closed network, which is open to flows of energy and resources. It has a networked structure where the SEEAs of all levels of territorial organization (from global to local) are interconnected. According to Bateson14 , each individual SEEA can be regarded as a “metapattern,” which is a system-forming and structuring core for informational and territorial systems of resource use and environmental protection.

As a networked structure, the global SEEA (though as yet insufficiently structured) is gradually being assembled from similar but at the same time different (depending on broadly conceived geographical conditions) SEEAs from various levels of territorial organization (country, region, local territory). If the SEEA is viewed in terms of and through the tools of fractal geometry15 , one notices an amazing feature: in the development of environmental-economic accounting specific patterns are repeated over and again at descending levels, such that their parts at each level appear to be a whole.

The fundamental significance of an integrated approach, which is implied by the systems concept of Life, tends to elude the attention of researchers. This is seen, e.g., in the attempt to develop primarily industrial rather than territorial SEEAs. The former, despite their obvious topicality, fail to address the integrated development of territories and do not make it possible to select the best options for resource use (judged by environmental and economic criteria).

Without an integrated territorial approach to the development of SEEAs, one cannot integrate them in the measurement of ecosystem service flows, the very concept of which, introduced in the report Ecosystem Evaluation on the Threshold of the Millennium (Millennium Ecosystem Assessment, 2005), substantially changed the tenor of ecological discussions, including discussions of biodiversity conservation. The evaluation of ecosystem services paves the way for implementation of a number of conceptual provisions that are critical for including the high economic value of specially protected areas (SPAs) in the natural capital of territories, so that the respective indicators can be accounted in the SEEA (Cadaster Institute, 2006b; 2011; 2012b; 2014; 2015a).

The understanding of the SEEA as a system-forming territorial core, a metapattern of information systems in the sphere of resource use and environmental protection, makes it methodologically untenable to assert that raising the quality of all indicators is a prior condition for the SEEA to be successful in any country. In reality, an attempt to raise the quality of indicators across the board leads to a lengthy and costly process of national statistics reform, postponing their systematic analysis. In our view, such an (essentially Cartesian) approach is at variance with the logic of the systems concept of Life and thus with the theory of sustainable development. So every country or region should, at the initial stage of work on an SEEA, systemically evaluate information sources as to the completeness, validity and accessibility of indicators. As practical experience has shown, the restricted character of traditional statistical systems16 makes it necessary to expand the range of data, which are handled, beyond official statistics, making use of administrative and expert data as well.17 It is particularly important to determine the trustworthiness of individual indicators and the system as a whole, identifying data gaps and finding ways to improve their quality (pilot field studies, calculations, adjustment of the available data, etc.) The process should begin with the preparation of basic territorial accounts (matrixes, which are the foundation of the SEEA), even if some indicators have to be accepted as expert assessments, and even if it is not possible to make a representative cost estimate. Completion of SEEA matrixes in physical terms provides useful information for comprehensive resource use and environmental management.

Our experience in multiple studies regarding the application of SEEA methodology at different government levels (federal, regional, municipal and micro-level) showed that the new systemic approach to obtaining and using indicators of natural capital and its components (even if the indicators were no more than expert assessments in some cases) broadens the potential for analyzing data on environmental resources and ecosystem services as a part of national, regional and even local wealth, and as an important factor for the sustainable development of territories. SEEA methodology can provide comprehensive information for appraising efficiency in the management of natural capital and efficiency of budgeting as applied to environmental management. It also becomes possible to analyze dynamics of the environmental resource stock in a specific territory and measure to what extent the environmental capacity of the territory can meet the resource needs of its economy.

-

Having acknowledged the multiplicity of possible futures, we need to identify and assess the different scenarios and trends based on criteria of sustainable development and determine which of them represent a hazard for human beings and ecosystems. Acceptance of the need and expediency of certain restrictions in order to avoid negative trends entails special importance of indicators that measure environmental impact and green growth (describing processes between the environment and the economy). Therefore, when estimating the amount and structure of natural capital for purposes of the SEEA, indicators are needed, which identify the risk of dangerous depletion, in both its environmental and social aspects. This highlights dangers timely and helps to find ways of meeting budget and public income shortfalls, thereby preventing conflicts in environmental management before they can become critical. Depletion of intensively exploited natural resources (mainly non-cultivated resources, such as fish and game, forest resources or mineral and energy resources, as well as water resources) can lead to substantial loss of household incomes, exacerbating environmental problems and conflicts. Resolving this problem is of crucial importance for sustainable development and it is specifically mentioned in the WTO regulations, which do not preclude measures for “the prevention of natural resource depletion.” It should, however, be possible to avoid such measures from becoming a “covert limitation on international trade” or a “discriminatory” measure; they must be applied alongside limitations on domestic production or consumption (art.XX(g) WTO/GATT Agreement)

-

Change in the concept of “sustainable resource use” by accepting its multifaceted character and, at the same time, the unity of forms of rationality expands our understanding of environmental-economic interrelationships as relations within an open, non-equilibrium system. Accepting the unity of rationalities makes it absolutely inappropriate to be skeptical about other forms of rationality (inherent to other civilizations and nations, or other historical periods), provided that such forms of rationality do not destroy the system of Life on Earth.

Adoption of the Sustainable Development Goals by the UN General Assembly 2015 should intensify the convergence of rationalities as regards environment management based on sustainability. This means that new system links are being formed, oriented to preserving Life on the Earth, which motivate and define how information systems can be created for sustainable resource use and environmental protection.

For many modern communities a change of tack towards sustainable development entails a shift in perception and transfer to systems thinking: from parts to the whole, from objects to relationships, from content to patterns. This evidently applies to the SEEA, which is an important element of sustainable development. At the same time, the importance of educating people about sustainable development becomes paramount, since implementation of the SDGs requires system changes in society, and that can only be achieved by nurturing a sense of responsibility 18 among people and in communities.

-

When measuring relationships in the Society – Nature system, the SEEA proceeds from the multiplicity of interconnections within communities. To respect the sustainability of communities is to respect these relationships. According to Capra (2003), reintegration into the life web depends on the establishment and maintenance of sustainable communities, in which we can satisfy our needs and wants without detriment for future generations.

Clearly, the establishment and maintenance of sustainable communities requires changes to information systems and indicators. Today, an SEEA is what makes it possible to measure various processes in territorial environmental-economic system and to measure socio-cultural specifics of different nations, which restrict and regulate useful institutional changes. This can be done with the help of the SEEA, using ethnometrics and humanization of monetary estimates of environmental resources (Fomenko G., 2014; 2017). The flexibility of the SEEA enables new Society-Nature measurements to be included into the systems analysis. We believe that alignment of the SEEA with socio-cultural measurements should be a research priority.

The SEEA methodology for preparing accounts permits extension of physical reporting on the use of natural resources to the sphere of the non-observable economy (by generating so-called “shadow” accounts), while the methodology of economic valuation (based on the theory of full economic value) enables researchers to discover subjective assessments of specific environmental resources and behavioral aspects of resource use. The latter expands the scope of economic evaluation in accordance with the actual value of natural resources for users, taking account of socio-cultural, non-economic values and thus providing important information for making effective managerial decisions.

-

It is important, when developing an SEEA, to realize that the main conflict between the industrial economy and ecology stems from the fact that nature is cyclical while industrial systems are linear. According to the systems theory of Life, sustainable patterns of production and consumption must acquire a cyclical character, similar to that of natural processes (Capra & Luisi, 2014). The European Environment – State and Outlook 2015 report discusses the problems of environmentally unbalanced systems of production and consumption and their long-term and often complex impact on the environment and on people’s health. The authors stress that society obtains many benefits but inflicts damage on the environment due to our linear economy based on the principle “buy – use – dispose,” our huge reliance on many natural resources, an “environmental footprint” that exceeds the planet’s capabilities, unfavorable impact on the environment of poorer countries and unequal distribution of the social and ecological benefits provided by globalization. It is clear that any long-term solution must be based on the transformation of major systems: transport, energy, utilities and food.

It has become clear that the achievement of sustainability depends almost completely on the creation of an economy of a special type, where growth of human well-being is combined with reduction of risks for the environment. Such an economy is called a “green” economy. The most common definition is the one given by UNEP: “the green economy is one that results in improved human well-being and social equity, while significantly reducing environmental risks and ecological scarcities.” The concept of effective resource use is directly associated with this.

The SEEA has to be developed in a way that makes it responsive to the processes involved in transition to the green economy. Firstly, there has to be support for various structures and functions of ecosystems (ecosystem sustainability) and ways must be found of reducing the use of resources in production and consumption and of mitigating their impact on the environment (resource efficiency) (Fomenko G., 2011).

-

According to the systems theory, ecosystems and human communities are always at risk of destruction, should their fluctuations exceed the tolerable limits, so that the systems are unable to compensate. If, e.g., someone tries to maximize any individual or group variable, this will inevitably result in destruction of the system as a whole. Therefore, timely identification and warning of a dangerous state of the Society – Nature system is increasingly understood to be the crucial condition for the efficiency of information systems, including statistical systems.

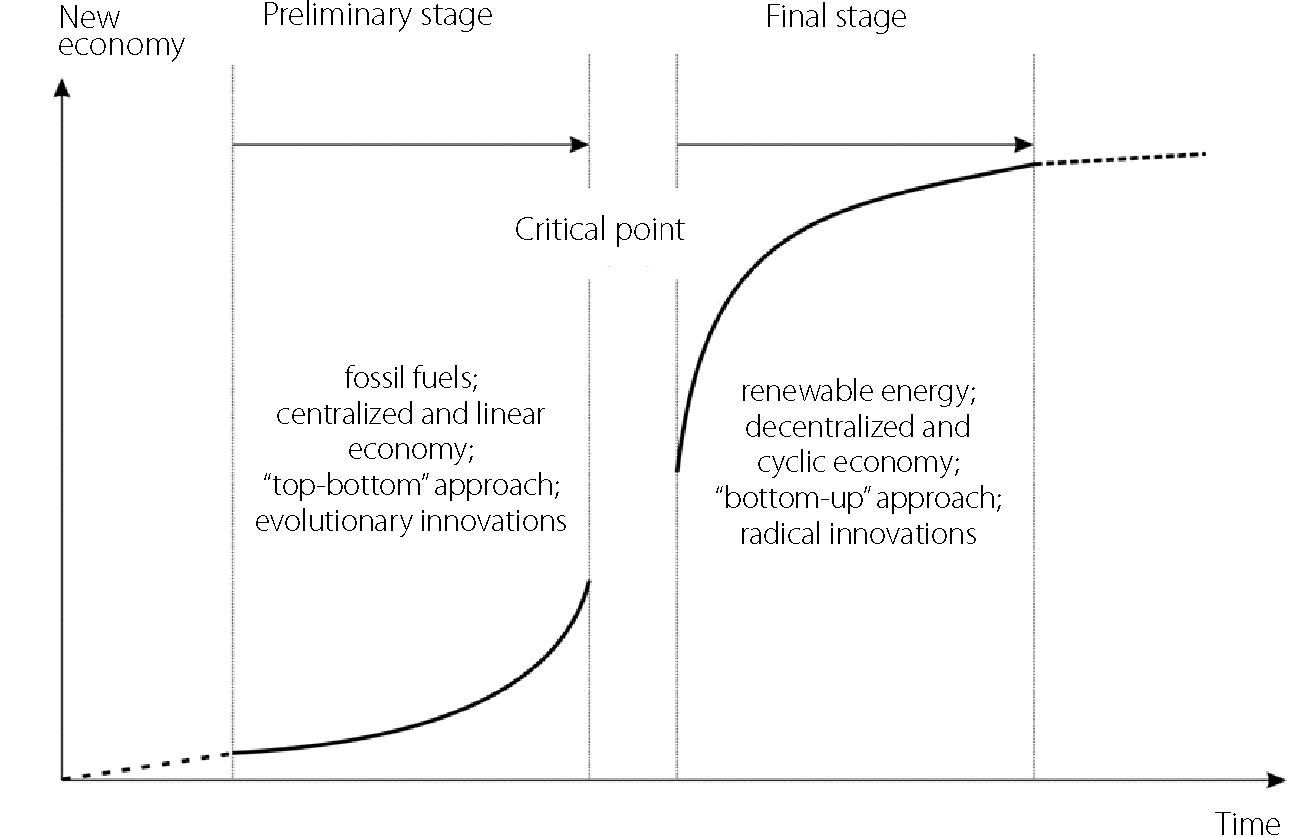

Particular dangers arise if a bifurcation point19 is passed, which is a critical state of the system, so that the system becomes unstable in its fluctuations and uncertainty arises whether the state of the system will turn chaotic or whether it will ascend to a new, more differentiated and elevated level of regularity. Attention should be paid to the position of many leading experts whose opinion was voiced most coherently by Rotmans at the Green Growth and Sustainable Development Forum 2015 (Enabling the next industrial revolution: Systems innovation for green growth, OECD). In his report “Transition to a Low Carbon Economy: How to Accelerate the Transition?” Rotmans states that the transition to a new economy has today reached a critical point (Fig. 1.2) involving chaos, conflicts and the spread of hostilities in various regions20

Fig. 1.2 Features and Dynamics of Transition to New Economy

The bifurcation point cannot be successfully passed unless the system has sufficient flexibility. According to the systems Life theory, all observable ecosystem variables (population density, access to nutrients, weather patterns, etc.) always fluctuate, as do the conditions of society and production. The Life web is a flexible fluctuating network. The more variables are involved in fluctuations, the more dynamic and flexible the system is and the greater its ability to adapt to changing external conditions. Low flexibility of a system is manifested by stress; notably, stress arises when one or more variables characterizing development sustainability approach their extreme values, heightening the level of rigidity and stress throughout the system. According to Capra (2004), prolonged stress is harmful and destructive for the system, while temporary stress is an indispensable feature of life. Environmental fluctuations in the stable state do not go beyond permissible limits even though disturbances in the Society – Nature system occur all the time and the network responds to them by recurrent fluctuations. In the stable state measurement of processes occurring between the economy and nature is effective and helps to reveal trends by the application of linear prediction methods.

When the world is passing through a bifurcation point related to technology transition to a new economy, we observe a crisis in measurability: the existing statistics and industrial information systems, which have been used to measure development trends in the departing era, miss the new growth trends and fail to identify threats to sustainable development. This makes new demands on the SEEA methodology and its implementation, particularly for greater sensitivity to new growth features. Important criteria of SEEA efficiency are:

1) flexibility, i.e., ability to “see” emerging new development trends in the Society – Nature system and to measure them;

2) ability to obtain necessary and sufficient information to control environmental and economic safety criteria, non-observance of which leads to destruction of the system, and to search for optimal values of the system’s variables.

The System of National Accounts is an internationally coordinated standard set of recommendations to measure indicators of economic activities in accordance with strict rules of accounting and reporting at the macro level. The system is based on the principles of economic theory and in its general form is a detailed report on economic activities in a country and on the relationships between various economic actors and groups of actors in markets or outside markets. Those recommendations are worded as a system of concepts, classifications and rules of accounting, which make up an internationally coordinated standard for calculating gross domestic product (the most commonly used indicator of economic performance). The SNA methodology calculates and presents economic indicators in a format that is specially designed for the purposes of economic analysis, decision-making and the preparation of economic policies. The accounts contain a large amount of detailed information organized according to the principles of economic theory and approaches to functioning of the economy (SNA, 2012, chapter 1, paragraph 1.1).

The conceptual basis of the SNA consists of accounts that are:

- inclusive of all kinds of activities and their consequences for all economic actors;

- mutually coordinated, since they use identical values and the same rules of accounting in order to establish the impact of one action on all parties involved in the economic process;

- integrated, because all consequences of the action of one subject are necessarily reflected in the resulting accounts, including balance sheets which show the influence of the actions of subjects on wealth measurement (SNA, 2012, chapter 1, paragraph 1.1).

In this way, the SNA fulfills an important informative and analytical function, structuring blocks of statistical information and answering the generalized questions: what happened in the economy? what actors participated and for what purposes? The SNA focuses on the measurement of production of goods and services (SNA, 2012, chapter 1, paragraph 1.6) and this predetermined its basic conceptual elements: institutional units and sectors; transactions and other flows; assets and liabilities (or stocks); products and units that produce them; goals.

Assets and liabilities are components of the balance sheet for the economy as a whole and for institutional sectors. The balance sheet shows stocks of assets and liabilities owned at a certain time by an individual unit or sector or by the economy as a whole. Balance sheets are usually prepared at the beginning and end of the reporting period although they can be prepared at any time. Stocks arise from accumulation of the outputs of previous transactions and other flows and they are also affected by subsequent transactions and other flows. So stocks and flows are closely interrelated (SNA, 2012, Chapter 2, paragraph 2.33).

Generally, an asset is an accumulated stock of value providing the owner with economic benefits or a number of economic benefits that arise from its ownership or use during a certain period. It is a means for the transfer of value from one reporting period to another. All assets in the SNA are economic. (SNA, 2012, chapter 10, paragraph 10.8). The relevant assets are those in some form of ownership and whose economic benefits are obtained by their owners through owning them or using them in economic activities as stipulated in the SNA. Accordingly, durable consumer goods, human capital and environmental resources, which cannot provide economic benefits to their owners, are not included in the scope of assets in the SNA.

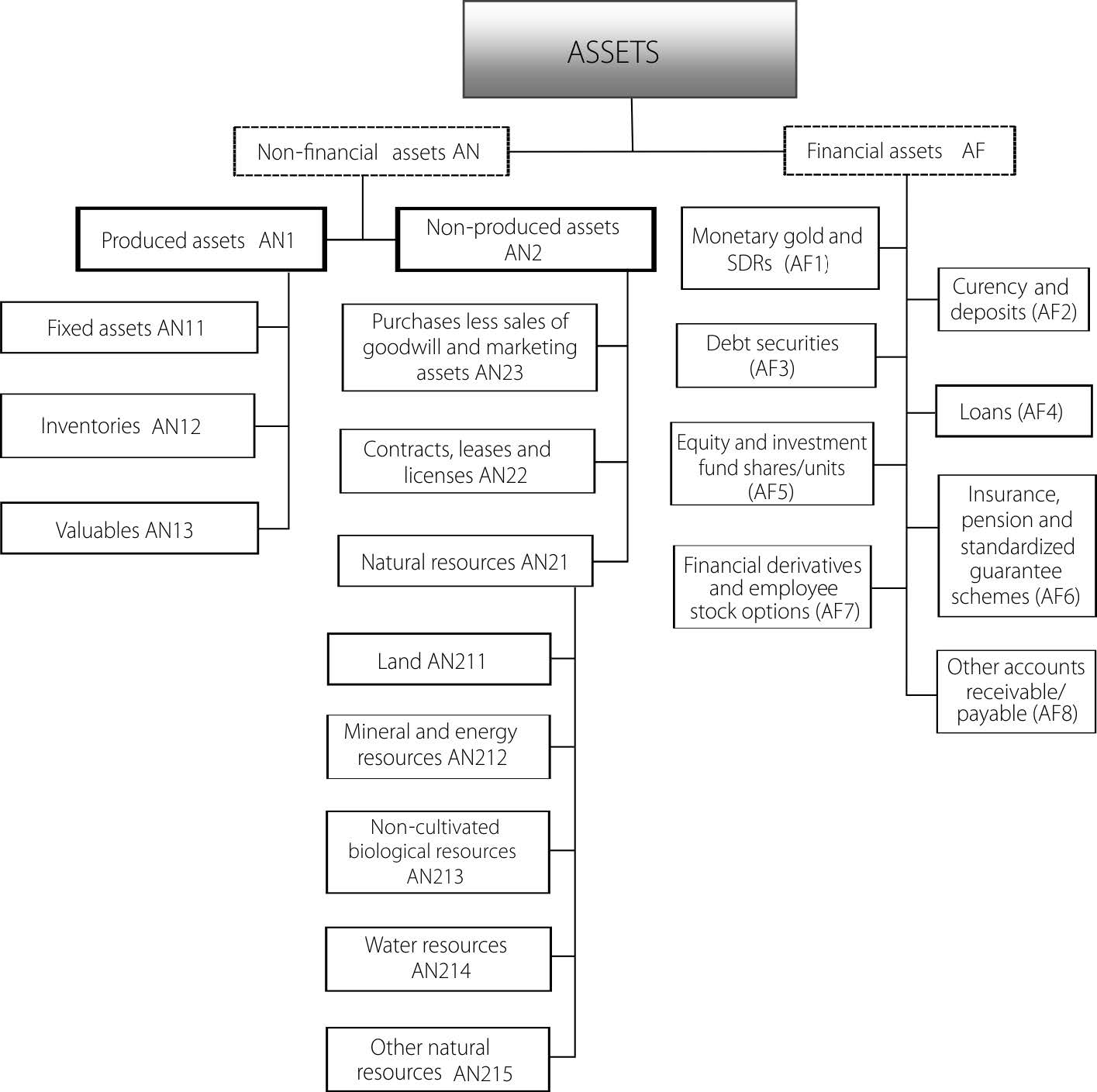

Classification of assets at the first level distinguishes non-financial and financial assets (Fig. 1.3). Non-financial assets are mainly represented by items, which can be used in economic activity and which are simultaneously stocks of value. Financial assets are mainly stocks of value.

There are two categories of non-financial assets:

- products created by production processes within the sphere of production defined in the SNA;

- non-financial assets, which have come into being by other means than production processes. Non-produced assets consist of three categories: environmental resources; contracts, lease agreements and licenses; and acquired goodwill and marketing assets (SNA, 2012, Chapter 10, paragraph 10.14). Environmental assets are resources of natural origin, such as land, water resources, forests and mineral resources, which have economic value (SNA, 2012, Chapter 10, paragraph 10.15).

Detailed examination of the methodological premises of the SNA 2008 on environmental resources shows that not all of them can be classified as economic resources.

Fig. 1.3 General classification of assets in the SNA

Firstly, the SNA only records assets owned by institutional units22 , i.e., only resources with established ownership rights, the observance of which is ensured, are qualified as economic assets. It is important, in this respect, to distinguish between legal and economic ownership. A legal owner of items, such as goods and services, environmental resources, financial assets and liabilities, is an institutional unit having a statutory right to claim economic benefits related to those items. By contrast, an economic owner of items, such as goods and services, environmental resources, financial assets and liabilities, is an institutional unit having the right to claim economic benefits related to the use of the above items in the course of economic activity by assuming the associated risks (SNA, 2012, Chapter 10, paragraph 10.5).

Environmental resources, being non-financial non-produced assets, can be owned by private, public and other owners. Some of them, being public goods, cannot be recorded in the SNA because it is impossible to establish the ownership rights attaching to them (e.g., atmospheric air, oceans, etc.). This is also true of resources that cannot be actually owned by any specific institutional unit, notably, resources whose existence is unknown or which are known but are so remote and inaccessible23 that they are not effectively controlled by any institutional units. Numerous institutional studies in the sphere of natural resources and ecosystem services have found that serious difficulties in defining boundaries and evaluating assets are mainly due to the fact that ownership rights to natural resources are historically uncertain and not embedded in people’s minds (Fomenko G., Fomenko M., Arabova, Ladygina, 2013; Fomenko G., 2014). Therefore, situations related to the use of environmental resources require an analysis of interest groups.

Secondly, in order to be defined as economic assets, environmental resources have to provide economic benefits to their owners, taking account of technology, scientific expertise, economic infrastructure, available resources and market conditions. Therefore known stocks of resources (e.g., mineral deposits or food resources), the use of which will not be commercially viable in the foreseeable future, are not considered in the SNA to be economic assets. That is the case, despite the possibility that such stocks may later become commercially viable due to some unforeseen technology breakthroughs or material change of market prices. Biological resources that are classified as rare or threatened with extinction, and which are under government protection and generally excluded from economic exploitation are also not considered being economic assets.

So the System of National Accounts treats environmental resources as physical non-produced assets. They are reflected in accounts when they are owned (legally and economically) by institutional units and used by their owners for economic benefit. Data concerning such resources are reflected only in monetary terms; indicators of their stocks and use in physical terms (cubic meters of water and timber, wildlife populations, etc.) are ancillary and are employed in the SNA solely for obtaining monetary values. This approach inevitably reduces opportunities for analyzing the stock and use of environmental resources in all their variety and wealth; in particular, it fails to discover risks of depletion and, generally, cannot meet the needs of sustainable environmental management.

The first attempts to include data on consumption of natural resources in economic analysis were undertaken as early as the 1930s when accounts were created that embrace all indicators of economic activity, based on the theoretical work of Marshall, Keynes, Clark, Stone and others. Later, in the late 1960s, the results of research enabled the formulation of radically new approaches to the construction and the functioning of statistical systems by uniting accounts based on different kinds of capital (economic, environmental, human). This signaled a new understanding of the need to include environmental assets in national accounting systems, reflecting their major role in sustaining human life and the economy.

The UN Summit on sustainable development in 1992 proposed development of a system of integrated economic and environmental satellite accounting (Agenda 21, 1992) in furtherance of these pioneering works and in order to provide a more detailed record of environmental factors in the SNA, thus providing an adequate picture of relationships between the economy and the environment, which could be used as a basis for accumulating data on the available stock of environmental resources and their depletion through use. The first set of guidelines for environmental-economic accounts, published in 1993, contained basic principles for implementation of a supplementary system of integrated economic and environmental accounting, describing relations between the environment and the economy. The following years saw intensive efforts to improve methodology and practical approaches to formation of the SEEA as a critical and integral part of the SNA; guidelines for economic and environmental evaluation of fish, water, energy resources and ecosystem services were developed and approved (UN, 2012b; SEEA, 2015). In its present form the SEEA has solid methodological foundations, despite certain deficiencies of a theoretical and applied character (UN, 2014).